{kind=link}

{kind=link}

{kind=link}

Retirement is one of the biggest phases in your life — and, as such, should require a good chunk of your attention to ensure you can reach your goals worry-free.

You’ll face a lot of financial hurdles, choices and decisions as you close in on that day, and along the way you’ll have to be flexible with those choices depending on your investments, health, family requirements and other factors.

According to a 2020 Board of Governors of the Federal Reserve System report, retirees make up a good portion of the population — 27 percent of adults in 2021 considered themselves to be retired, even though some were still working in some capacity. In deciding when to retire, most people indicated that personal preference played a role, but life events — health reasons (including COVID-19), family requirements, or forced retirement — contributed to the timing for 45 percent of retirees. Forty-nine percent of retirees said a desire to do other things or to spend time with family was important for their decision to retire, and 45 percent said they retired because they reached a normal retirement age.

Nonetheless, 29 percent said that a health problem was a factor in their decision to retire, and 15 percent said they retired to care for family members. One in 10 said they were forced to retire or that work was not available.

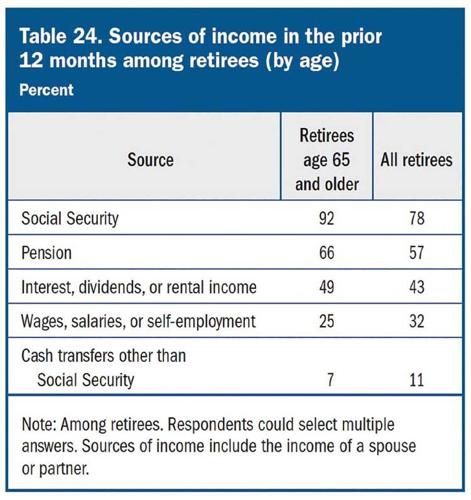

The report also notes that Social Security was the most common source of retirement income, but 79 percent of retirees had one or more sources of private income — 57 percent had a pension; 43 percent listed income from interest, dividends, or rental properties; and 32 percent still had income from a job.

In 2021, 81 percent of all retirees said they were doing at least okay financially, and 60 percent reported high levels of life satisfaction. Retirees with a disability were less likely to report they were doing at least okay financially or that they had high levels of life satisfaction. So between Social Security and a few other sources of income, most folks can bring in enough income to reach their goals.

We consulted with dozens of reports from retirees, government sources and wealth management professionals for a few tips you can consider as you close in on retirement.

• Plan for the unexpected. One reason to think ahead to retirement planning: You may be forced to retire early, either due to an unforeseen health problem, by forced retirement/layoff/ business closure, or to take care of a family member. According to a recent survey by the Employee Benefit Research Institute, almost 30 percent of respondents said they expect to work until age 70, but only 7 percent make it that long.

• Find a wealth and retirement investment professional. Finding someone you trust is important, since you’ll be working with this professional for the rest of your life. They’ll help you figure out a budget, walk through your income sources and expenditures, will work with you to navigate major events such as IRA rollovers and withdrawals, and assist you in calculating when you can start drawing from your investments and when and how you should be using personal savings — along with the annual amount you should tap into to minimize your tax hit.

“Self-directed retirement accounts frequently have complex rules on withdrawals and rely on individuals to have the skills and knowledge required to manage their own investments,” the Fed report on retiree trends states. “Non-retirees with self-directed retirement savings varied in their comfort with making investment decisions for their accounts. Nearly 6 in 10 non-retirees with self-directed retirement savings expressed low levels of comfort in making investment decisions with their accounts.”

• Have a plan for retirement. Whether it’s travel, more time with the kids and grandkids, picking up a hobby, volunteering, gardening, connecting with friends or putzing around the house, you’re still going to need some type of annual budget to follow so you can check your short- and long-term goals versus the reality of your retirement income. After your initial assessment, it could be a perfect time to prepare yourself by phasing out some discretionary spending habits that’ll save money now and in the future — non-essential spending binges, subscriptions to streaming services you don’t use, luxury travel, and overreliance on dining out.

Even small changes and spending controls in your current lifestyle can pay off down the road. “If you look at everything you purchased over the course of a month, you may be surprised at how much you can cut back to have more money to invest for your retirement,” says Debra Greenberg, director, Investment Solutions & Personal Retirement, Bank of America.

Create a worksheet with your annual spending in retirement. You can do this on your own, and it will also be one of the first exercises you do with a financial planner. A professional can walk you through dozens of retirement scenarios, helping you define costs compared to the bulk of your projected investments and matching it up with your investing preferences to provide you with a clearer idea of how much you can expect to have 20 years into retirement, and what you’ll need to get to your other aspirations.

A typical worksheet would include regular expenditures such as house and car payments, insurance, health and prescription costs, utilities, phone, even monthly entertainment allowances. These exercises can account for major expenditures you’d plan for, such as replacement vehicles, cruises or other major trips, vacation property purchases, new hobby expenses and potential big-money layouts that would impact your funds.

Other factors would include start dates and projected monthly payouts for Social Security benefits, annuities, pensions, insurance settlements, and other scheduled income. Too, long-term factors would include final payoff of a mortgage or car payment.

Ultimately, it’s critical to be on the same page as your spouse and financial planner. The more you can account for early on and avoid surprises, the better off your plan will be.

• Inflation isn’t going away. Ever-increasing costs and inflation can erode your future investments — while 15 years ago a static $100,000 in savings may have looked like a relatively comfortable cushion, today it may only last a few years once you tap into it because the substantial increase in costs of … well, everything. Financial planners have inflation factors built into their projection models as you map out your retirement needs.

• Health will be an important focus. Health insurance isn’t getting any cheaper, and a serious health setback or even a need for home health care or assisted living early in retirement can mean a catastrophic hit to your resources — especially since Medicare/Medicaid likely won’t cover all of it (such as long-term care costs). According to a Nationwide Life Insurance report, the required annuity to cover out-of-pocket health care costs was about $206,000 per couple in 2010; it’s projected to be nearly $492,000 in 2040.

You can do your part by keeping yourself mentally and physically fit, following a good diet, getting regular physicals and dental checkups, and looking into insurance plans that can potentially cover assisted living costs.

Before retirement, it’s a good time to address medical issues while you’re still on company insurance. Foot surgeries, arm soreness, dental issues you’ve been putting off — get in to see a specialist (and your own current medical providers) before you’re off the corporate plan.

Another thought, depending on your current health, might be to look at long-term care insurance, which can come in handy for home health care. Getting coverage early will probably mean lower premiums now, along with a better likelihood of being accepted by insurance firms.

And if you’re in a health plan that lets you contribute to a health savings account, consider maxing out your current contribution. The money can build (with tax-free compounding interest) until you need it for qualified medical expenses after age 65.

• Considering squeezing in a few expensive one-offs before you retire. In the five years leading up to planned retirement — with the caveat that you’ve been planning for these big events and have checked in with your financial planner — it might be a good time to get major cash-eating projects completed, such as a remodel, buying updated furniture, or going on one last massive family trip.

And if you can swing it, consider paying cash for these major outlays — or at least avoid a multi-year debt. By working off old debt such as mortgages and car payments and avoiding new credit card charges, you minimize the amount of retirement income that might be spent on interest payments. “If you pay off a credit card that charges 15 percent interest, it's like earning 15 percent on a risk-free investment," says Anil Suri, managing director in the Chief Investment Officer at Bank of America.

• If you’re concerned about your retirement nest egg, you can still work longer or work part-time. The inflationary cycle we’re in — along with the recent pandemic and job concerns — have some soon-to-be retirees concerned about their financial status (see sidebar). However, a major trend among recent retirees is to work past the age at which they’d already planned to retirement. Bringing in that extra cash flow for a few years can help you stave off tapping into your nest egg, and may help you delay Social Security payments (which will lead to larger Social Security benefits when you do use it.) MKE

Retirement Worries

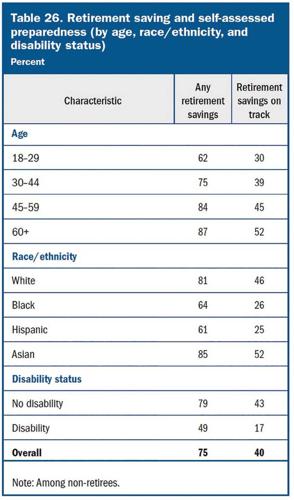

The uncertainty in rising costs has led to a certain amount of angst for workers, even those close to retirement. According to a U.S. Department of Labor survey, 62 percent of U.S. citizens have retirement savings, but less than half feel they’re on track to retire by age 65.

Age | Any Retirement Savings | Retirement Savings On Track |

| 30 to 44 | 75% | 39% |

| 45 to 59 | 84% | 45% |

| 60+ | 87% | 52% |

| Overall | 75% | 40% |

And according to a July report from the National Institute on Retirement Security (NIRS), the outlook for Generation X — the first generation to enter the labor market following the shift from defined benefit pension plans to 401(k)-style defined contribution accounts — is even more morose. When looking at median retirement savings levels for Generation X, the bottom half of earners have only a few thousand dollars saved for retirement, and the typical household has only $40,000 in retirement savings. Skewing the data even further, retirement savings for Generation X is highly concentrated among the highest earners, while Blacks and Hispanics have substantially lower savings and access to retirement plans as compared to whites.